Market and regulatory issues related to Bio-CCUS

Publications

Market and regulatory issues related to Bio-CCUS

Introduction

The fourth IEA Bioenergy Task 41 workshop on Bio-CC(U)S was organized in Brussels 16 January 2018. The topic of the workshop was Market and regulatory issues related to Bio-CCUS. The workshop was a full day event divided into four consecutive sessions:

- Background and introduction: The session focused on bioenergy, bio-CCS/BECCS in general and as business cases, and the natural climate mitigation potential of forests. The session also included an overview of the importance of bioenergy with CCS in the recently published IEA Bioenergy Roadmap.

- Policy perspectives: The session addressed different policy perspectives related to Bio-CCUS/BECCS and identified a set of gaps and opportunities including bottlenecks in Bio-CCS regulation.

- Bio-CCS and Bio-CCU: The sessions on Bio-CCS and Bio-CCU addressed industrial experience and industrial potential of Bio-CCS, including waste-to-energy, forest industry, biogas production, and microalgae production.

- The workshop was rounded off with a panel discussion led by Adam Brown from IEA. This report gives a brief summary of the workshop.

The objective of the workshop was a) to increase knowledge on the topic and contribute to the definition and establishment of terms drivers and impact mechanisms of the Bio-CC(U)S technologies, and b) to gather viewpoints of how different industrial sectors, governments and institutions see the implementation of these technologies.

BECCS and BECCU in the IEA Bioenergy Roadmap

Regardless of the expansion of renewable energy sources such as wind and solar over the past years bioenergy continues to dominate the renewable share of the global final energy consumption. In the updated IEA Bioenergy low-carbon scenarios presented in the Energy Technology Perspectives 2017 bioenergy is an essential component. In the 2°C scenario (2DS) bioenergy is responsible for 17% of the total cumulative CO2 reductions by 2060. The share increases by 22% in the Beyond 2°C scenario (B2DS), including BECCS (see Figure 1). The IEA scenario modelling applies a cap on bioenergy primary energy supply of 140 EJ.

Figure 1 The role of bioenergy in the IEA low-carbon scenarios (IEA, 2017)

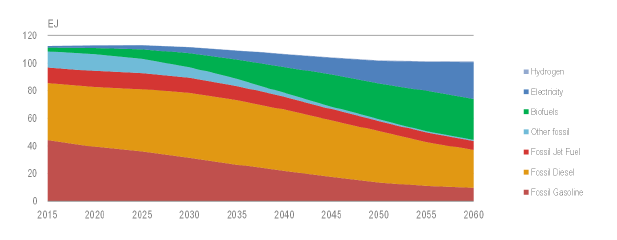

Currently bioenergy accounts for around 18 EJ of final energy consumption. The main utilization of bioenergy today is for industry and heating of buildings. Transport and electricity generation are smaller sectors. Over the next decades, the allocation of bioenergy in these sectors will probably see a radical change as consumption is estimated to increase to 73 EJ by 2060. The transport sector is projected to see the most significant change, with a tenfold increase in consumption up from 18% to 41% of the bioenergy in total final energy consumption, with a large majority of advanced biofuels. Biofuels will have a dominant role in the transport fuel portfolio of the 2DS in 2060. Even with a transport sector projected to double compared to current levels some 30% of transport energy is estimated to come from biofuels. Biofuels and transport electrification are strongly interlinked, and together these transport energy sources are expected to cut the use of fossil fuels in half as illustrated in Figure 2.

Figure 2 Transport fuel portfolio 2DS (IEA, 2017)

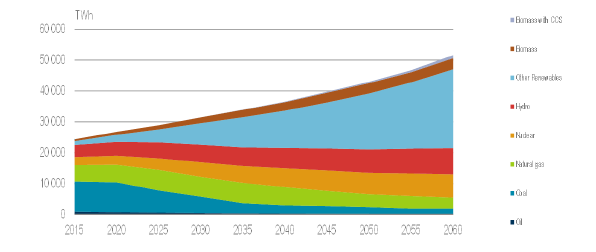

The advantage of biomass as an energy source is the opportunity to produce both biofuels and bioenergy (electricity and heat), thus serving two large energy intensive sectors. In the 2DS electricity generation is expected to double by 2060, and renewable energy excluding bioenergy is projected to generate around half of this electricity. Biomass still has a role to play and is expected to grow from 2% to 7%, as illustrated in Figure 3.

Figure 3 Electricity generation in 2DS (IEA, 2017)

Figure 3 Electricity generation in 2DS (IEA, 2017)

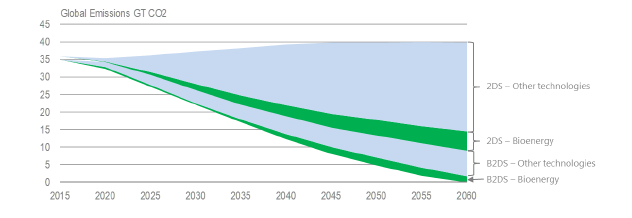

The role of bioenergy with CCS (BECCS) in the IEA Bioenergy roadmap plays a significant role in the reduction of future CO2 emissions. In the 2DS 34 Gt CO2 is projected captured by BECCS by 2060, 60% of this originating from transport biofuel production. In the B2DS BECCS is more prominent, with cumulative CO2 emissions reaching 72 Gt by 2060.

Figure 4 BECCS in 2DS and B2DS (IEA, 2017)

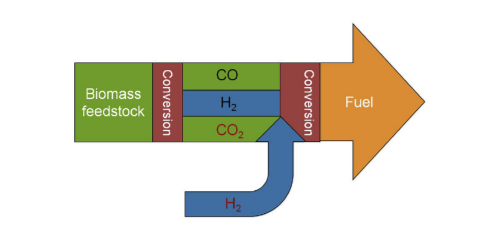

Bioenergy with carbon capture and utilization (BECCU), or recycling of the carbon, could also play a role in future emission reductions, especially in an established low-carbon society. A more efficient use of bioenergy would be producing both fuel and electricity. Adding low-carbon hydrogen into biomass conversion systems could convert more of the biomass carbon into fuel as illustrated in Figure 5. This option would not directly reduce the atmospheric CO2 concentration, but it would reduce the amount of biomass feedstock required to produce the same energy output and also reduce the need for extracting fossil fuels.

Figure 5 Using low-carbon hydrogen to increase biofuel production (Hannula, 2016)

One of the main conclusions from the IEA Bioenergy Roadmap is to accelerate things immediately. Some key actions include the promotion of short-term deployment of mature options (using established technologies such as for instance methane from waste), stimulate the development and deployment of new technologies (e.g. new transport fuels), sustainable generation of feedstock, including a supportive sustainability governance system, and spurring international collaboration in order to develop capacity and boost investment within a global regulatory framework. One of the most important measures to boost BECCS is to have a high enough carbon price to properly reward the double benefit of BECCS and less carbon intensive industry in order to force BECCS into the energy system. Also, technical support measures need to be available. For instance, a lot remains to be settled concerning the overall CCS infrastructure. These measures will require significant intergovernmental efforts. At the same time, the current progress is currently too slow to be able to realize the recent climate targets, and early policy action coupled with a high level of ambition will be crucial for industrial large-scale deployment of BECCS/BECCU.

Business cases based on negative CO2 emissions

The carbon reuse economy typically includes biotechnical upgrading, catalytic upgrading and thermochemical processes. Different drivers create sustainable business cases; decreasing CO2 emissions to mitigate climate change, the potential for new businesses, and expanding the resource basis and energy security of carbon.

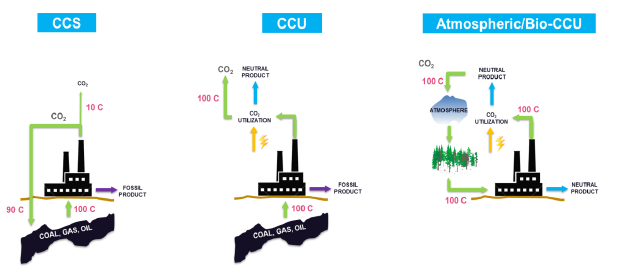

CCS and CCU are fundamentally different, as illustrated in Figure 6. In CCS the CO2 is captured and permanently stored underground. In CCU the captured CO2 is utilized as carbon feedstock in the production of energy carriers, chemicals and materials. As a consequence, the impact mechanisms of CCS and CCU on climate change are different. As CCU does not remove CO2 from the carbon cycle, CCU can at best be carbon neutral.

Figure 6 Carbon capture and storage vs. carbon capture and utilization

Figure 6 Carbon capture and storage vs. carbon capture and utilization

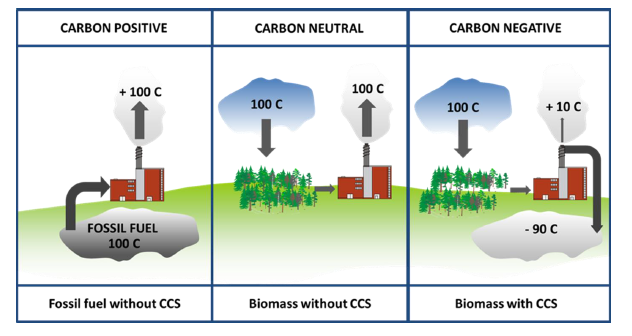

Figure 7 Different carbon capture concepts have different climate change mitigation impact

Business cases with near zero or even negative emissions can be established already now, and biomass-based industrial sectors are continuously striving towards carbon neutrality. Initiatives from the forest industry include more efficient use of side streams (e.g. lignin), expanding product lifecycle, production of fuels and chemicals to replace fossil fuels, development of new pulping processes and reforestation. Carbon negativity, on the other hand, can only be reached with Bio-CCS.

Hydrogen enhanced synthetic biofuels, as pictured in Figure 5, can also become economically attractive with a cost of low-carbon hydrogen below 2.2 – 2.8 €/kg. This type of Bio-CCU could play a role in processes relying on thermochemical conversion in the future, such as heat production, chemicals recovery, biomass-to-liquid (BTL) and biomass-to-X (BTX).

Climate change mitigation potential of forests

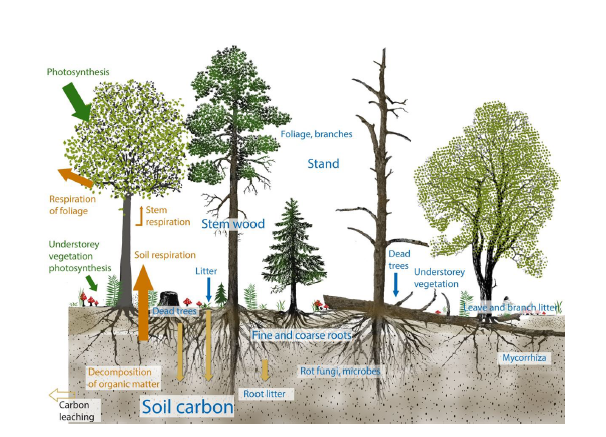

Forests are natural carbon sinks, utilizing atmospheric CO2 for the photosynthesis and stocking carbon during growth. Carbon is stored in both vegetation, vegetation litter and soil, but the carbon cycle of forests is a complex system and the exact carbon sink potential is uncertain. The type of forest strongly affects the carbon sink potential. For instance, there is a higher accumulation of carbon in boreal forests compared to tropical forests.

Figure 8 Carbon cycle in forest ecosystem

Greenhouse gas (GHG) emission in the EU are declining. From 1990 to 2016 the CO2-equivalent emissions were reduced from 5 700 Mt to around 4 400 Mt, a reduction of about 50 Mt CO2-eq. annually. That is well below the EU 2020 target calling for a 20% reduction. Increasing this positive trend, however, will be more challenging in the future. To reach the target of 40% GHG reduction by 2030 an additional 71 Mt CO2-eq. annually would be needed, a number increasing to around 114 – 157 Mt CO2-eq. annually to meet the 80 – 95% reduction by 2050. Currently, the EU forest sink is around 10% (~400 Mt CO2-eq./a). The carbon sink potential varies, and is dependent on regional and local conditions such as policies, economy and use of wood. In Finland, current GHG emissions amount to 55 Mt CO2-eq., while the land use, land use-change and forestry (LULUCF) carbon sink is 30 Mt CO2-eq. Harvested wood products, for instance, constitute a small carbon sink. More than half of the harvested forest volume in Finland is used in products with short lifecycles, such as pulp, paperboard and paper. Most of the carbon stored in wood products is stored in sawn wood.

Increasing the climate change mitigation potential of forests would require reduced logging, improved silviculture, controlling drainage on agriculture, reduced forest drain and establishing a LULUCF sink to offset emissions from food production. Also disturbances such as wind damages, bark beetles, forest fires, etc. should be minimized to maintain and increase the potential. In Europe only around 55 m3 of timber was lost to various disturbances from 2002-2010. On the forest product side a higher production rate of products with longer lifespan would increase the potential. This can be challenging as the demand for these products is driven by consumers.

Increasing the mitigation potential of forests is a slow process. It will take decades to achieve measurable results, and as a result, action must be taken soon in order to reach the 2050 targets.

Gaps and opportunities for BECC(U)S in current policies

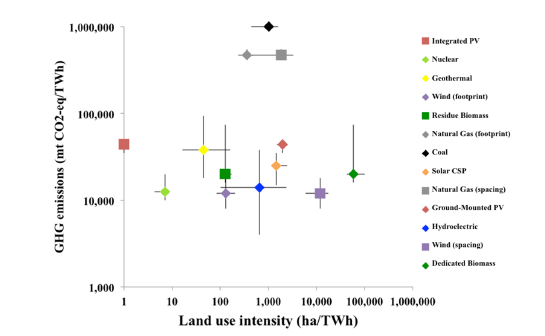

Bioenergy is of a complex nature including different potential feedstock types, different conversion processes and a variety of end uses and end users. For instance, the land use intensity of different energy sources shows that for instance biomass from crops utilized for electricity production requires on average 500 m2/MWh, while cellulose and forest residue for liquid fuel production requires only 0.1 m2/MWh. For comparison, the land use intensity of fossil energy resources is 0.1 – 0.4 m2/MWh (excluding surface coal extraction). Comparing the GHG emissions as illustrated in Figure 9, on the other hand, shows that the difference between GHG footprint for biomass and other energy systems (except fossil fuels) is not that high.

Figure 9 Land and GHG intensity

Embracing scenarios and possibilities that differ with several order of magnitudes depending on energy system, end use and regional conditions makes it impossible to talk about bioenergy in general terms. With this as a starting point, deploying large-scale Bio-CCS/BECCS may reduce the carbon emissions or even extract CO2 from the atmosphere, but the consequences of the associated land-use change and CO2 emissions could even offset part of the CO2 sequestered by Bio-CCS in the first place. A few large-scale Bio-CCS installations are currently operating, mainly from corn ethanol production where CO2 is collected and used in enhanced oil recovery (EOR). Apart from these projects in the US the overall performance of Bio-CCS has not yet been tested on large-scale, and both costs and public acceptance remain a challenge. The timeframe of sequestration, and thus the potential of carbon negativity also remains an important aspect; utilizing biogenic CO2 for fuel production, for instance, will not sequester the carbon for a very long time.

Accounting for biogenic carbon has not yet been established. Standardizing a purposeful method for biogenic CO2 accounting will be a major regulatory undertaking, especially if the CO2 is used as feedstock in other processes. Tracking the carbon in Bio-CCU will require a complicated cross-sectional approach between the various supply and demand sides.

Other challenges that are still to be balanced by regulation, although not exclusively associated with Bio-CCUS, include seismic risks, potential CO2 leakage and conflicting sub-surface land uses such as for instance extraction of drinking water and geothermal energy.

Bio-CCUS is only one alternative to sequester CO2. Other opportunities include afforestation and reforestation, sequestration into biochar and soil carbon, ocean fertilization (adding nutrients to the oceans in order to stimulate phytoplankton growth and increasing CO2 absorption), enhanced weathering (spreading CO2-absorbing minerals), and direct air capture (DAC). Some of these opportunities will have larger and more direct social implications, such as for instance afforestation and reforestation that could conflict with other land use. Also DAC could possibly interfere with other land use, depending on the size of the installation.

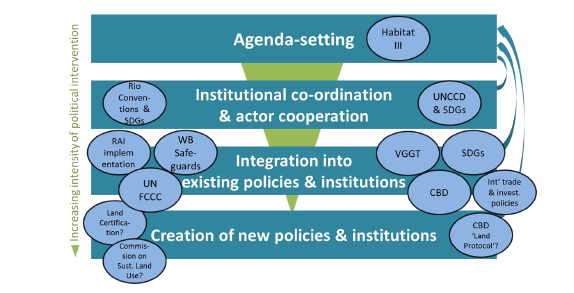

Regulating Bio-CCUS and land use is a stepwise process. Currently, several initiatives and activities address various steps of this process, as pictured in Figure 10. Few of these activities are systematized, resulting in an overall low efficiency. An important factor is the lack of knowledge about Bio-CCUS and its real effects.

Figure 10 Governing Bio-CCUS and use

Land use and CO2 sequestering opportunities such as Bio-CCUS could provide an interesting opportunity. A prerequisite would be that the raw material is sustainable, and in order for these two systems to purposefully interact a functioning governing system on land use change is needed. These systems would also need to be tested and demonstrated on a large scale.

Legal bottlenecks in Bio-CCS regulation

The main differences between conventional CCS and Bio-CCS relates to the definition of negative emissions, the accounting of the achieved emissions reductions, and the yet to assess impact of carbon removal technologies on biodiversity and the water-energy-climate nexus. There is sufficient legal basis to work on, but developing Bio-CCS will require significant political will and currently there is a lack of strong incentives and rewards. Three main challenges in regulating Bio- CCS relate to affirming its place in target compliance strategies, supporting the use of Bio-CCS technologies, and addressing environmental uncertainties related to such use:

-

- Target compliance: Binding emissions reduction targets remain the most effective incentive to adopt mitigation measures such as bio-CCS. Without such regulatory incentive, Bio-CCS may play its full role as mitigation measure. Bio-CCS also needs to be added to the policy agenda and be included in the target monitoring tools such as for instance Nationally Determined Contributions (NDC’s) or carbon budgets. Various UNFCCC documents refer to it, but new national policies refer explicitly to it. Indeed, the choice in favor of Negative emission technologies (NET’s) as a mitigation instrument remains at the discretion of the state. An additional challenge is the neutrality principle, which requires that support should be technology neutral.

- Enabling the use of Bio-CCS: Once the target has been agreed on the necessary regulatory adjustments should be made, including support tools and rewarding NET’s. Adjustments towards Bio-CCS should be based majorly on existing legal basis if possible (emission permits, EU ETS, CCS Directive, Renewable Energy Directive, etc.).

- Bringing legal consistency and certainty: Consistency is needed with respect to food, energy and water. Environmental uncertainties need to be dealt with. A precautionary approach should be taken to negative emissions and modifications of the atmosphere.

Policy and governance challenges of achieving negative emissions with BECCS

One of the key points of BECCS as a means to remove CO2 from the atmosphere is to consider the environmental impacts along the entire supply chain from biomass production through to energy generation and utilization. This comprehensive supply chain analysis ensures that the full environmental impact is addressed. However, such a comprehensive system scope comes with specific challenges related to for instance analytical perspective, ethical justifiability, and lessons learned from spatial ordering of bioenergy technologies (impacts across North/South borders or in global vs. local contexts).

Figure 11 Typical scope of Bio-CCS system analyses

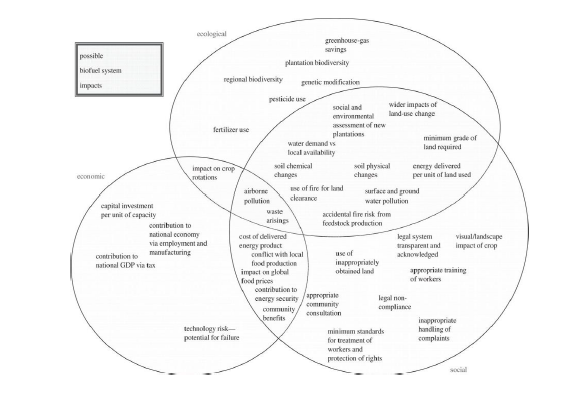

The typical scope of bioenergy system analyses is illustrated in Figure 11. This normally takes into account environmental impacts, but doesn’t necessarily serve to gain a true perspective of the entire system including its supply chain, or describe how the system behaves as an entity from a governance perspective. Bioenergy supply chains are heterogeneous systems, including ecological, economic and social impacts. Figure 12 illustrates the overlapping between these heterogeneous components and demonstrates their dynamic interaction. As can be seen from the diagram, especially social impacts overlap rather extensively both ecological and economic impacts. The interaction between ecological, economic and social components requires the consideration of a broader set of impacts beyond the environmental consequences of mitigating GHG across the entire supply chain as in typical sustainability lifecycle assessments (LCA) where spatial and human dimensions are often overlooked.

Figure 12 Ecological, economic and social spheres are overlapping

The Bio-CCS/BECCS supply chains are spatially ordered, and typically distinctly global. For instance, the UK target for bioenergy assumes a system of international trade of biomass commodity. Simultaneously, more impoverished nations produce and export biomass as a value-added energy product for more wealthy nations, which results in an environmental load displacement (North-South). This causes uneven spatial distribution with regards to which region(s) have benefitted from the system and which have had to tackle the negative impacts.

System models often conceptualize Bio-CCS/BECCS systems as a collection of technologies and resources, but the successful implementation of Bio-CCS/BECCS is also dependent on human dimensions including human-technology interaction, effects of social and cultural practices, and understanding the role of institutional and socio-economic innovations. In other words, public concerns about (Bio-)CCS is not limited to lack of knowledge and information, but can also be related to the way people value, use, interact with and depend on natural resources, energy products and services, and also how people perceive risks.

The comprehensive scope of system could be a significant challenge for Bio-CCS/BECCS governance. GHG emissions are a global issue, but the processes and possibilities to reduce them are typically dependent on national, regional and local conditions. Varying national GHG emissions coupled with different levels of integration in global supply chains and global emission treaties and protocols further complicates the scope.

Drawing on lessons learnt from the bioenergy discussion a mixture of Bio-CCS/BECCS policy measures sensitive to heterogeneity of local contexts and spatial impacts will be needed to account for negative externalities. Like in the case with bioenergy, a functioning Bio-CCS/BECCS economy will be dependent on a mixture of policy tools, and critical for Bio-CCS/BECCS will be policy-planning security and adaptive flexibility. The policy instruments should allow for flexibility to respond to new developments and changes in public attitudes while at the same time providing policy stability and planning security to provide market actors with confidence needed for investment. Including all stakeholders in decision-making processes would support the development of an adaptive flexible policy.

Carbon capture and storage in industry

WASTE-TO-ENERGY

Waste and waste handling is an increasing challenge with associated health, environmental and climate effects. Globally, around 4 billion tons of waste in generated every year. The city of Oslo is one of Europe’s fastest growing urban areas and was selected European Green Capital for 2019. In partnership with the city of Oslo the Klemetsrud waste-to-energy plant, owned by Finnish Fortum, is an important part of Oslo’s green shift. Receiving 400 000 ton municipal waste annually from the city the Klemetsrud plant produces 150 GWh electricity and 1.7 TWh of heat for district heating, serving more than 5 000 customers.

The Klemetsrud plant is part of the Norwegian state funded CCS project together with the Yara ammonia plant in Porsgrunn and the Norcem cement plant in Brevik. CO2 from the three plants will be shipped to the Smeaheia formation at the west coast of Norway for permanent storage. The CO2 will be delivered to a land terminal and pumped via pipelines to the aquifer. The storage part of the project is run by Statoil, Total and Shell in partnership. A total of 1.3 – 1.5 Mt CO2/a is expected from the three sources.

The flue gas from the Klemetsrud plant bear strong similarities to flue gas from coal-fired power plants. CO2 capture has been tested in a mobile capture unit, and test results show that 90% of the CO2 from the waste-to-energy plant can be captured. Electricity production would be somewhat lower, but the plan would still be able to deliver the same amount of heat to the surrounding city with a 90% capture rate. Of the CO2 emitted from the Klemetsrud plant, 55 – 60% are of biogenic origin, which would make the plant an industrial demonstration case of Bio-CCS, potentially also Bio-CCU in the future. The project is currently undergoing a Front End Engineering Design (FEED) study that is expected to be ready before summer 2018. Main challenges identified this far are high costs, immature supply market including lack of confidence in full-scale CCS chain realization, which again results in high cost estimates in the FEED study. Also public opinion could be a major obstacle; the transportation of CO2 from the Klemetsrud plant to the port in Oslo goes through a densely populated area. Communication with the public is currently ongoing.

The Norwegian government is interested in developing the CCS project and also has prospects of expanding abroad in the future. There are around 500 waste-to-energy plants in Europe, incinerating thousands of tons waste yearly. In addition, in the EU a significant part of municipal waste collected is dumped at landfills even though it could be used elsewhere, such as in waste-to-energy processes. Bio-CCS from waste-to-energy processes offers a significant potential and could represent a new business area for the sector.

PULP AND PAPER

The pulp and paper sector is the largest industrial user of biomass. A typical modern pulp and paper mill emits 75 – 100% biogenic CO2. Capturing and permanently storing this CO2 could contribute to negative emissions, provided that the biomass raw material is sustainably grown and harvested.

Retrofitting CO2 capture in the pulp and paper industry is technically feasible, and excess heat produced onsite can be used to power the CO2 capture plant. For a market Kraft pulp mill more than 90% of the total CO2 emissions can be captured with excess steam. For an integrated pulp and board mill additional energy is needed for high capture rates, for instance in the form of an additional boiler.

The retrofit of CO2 capture to an existing pulp and board facility is estimated to have a cost of avoided CO2 around 60 – 90 €/t, depending on the capture rate (higher capture rate reduces costs). This translates into an additional cost of pulp of 30 – 40%, which is a significant increase in product price. This radical price increase has potential to cause carbon leakage from the pulp and paper industry sector.

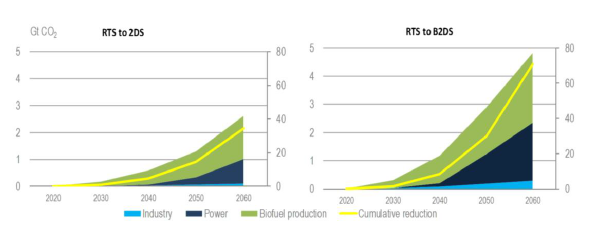

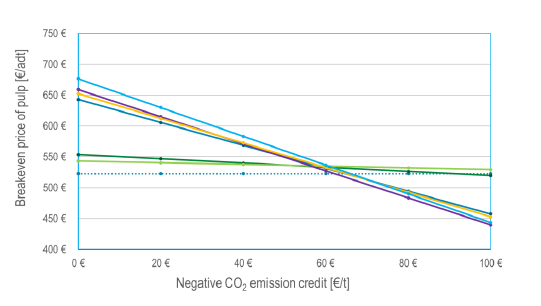

By allowing negative emissions in the EU ETS, incentivizing negative emissions through tax schemes, or otherwise rewarding negative emissions this could potentially become an additional income for the sector. Figure 13 shows an example of what it would possibly take to generate a new, additional income from negative emissions.

Figure 13 The effect of incentivizing negative emissions on the price of pulp

In order to reach a pulp price at the same level as before CCS retrofit a potential negative emission credit should be around 60 – 70 €/t (high capture rate cases, up to 90% of total site emissions). For example, a negative emission credit of 80 €/t would decrease the pulp price by 33 €/adt pulp, which translates into an additional profit of 26.5 M€/a. The example is estimated for a market Kraft pulp mill where 90% of total site emissions are captured.

The pulp and paper industry is, together with waste-to-energy as described above, a potential candidate for Bio-CCS and Bio-CCU demonstration, and could benefit from a scenario where negative emissions would be rewarded as part of climate change mitigation initiatives. The feasibility and realization of Bio-CCS in the forest industry is highly dependent on policies rewarding negative emissions, and long-term political stability that allows for investments.

COMPANY PERSPECTIVES ON BIO-CCUS IN FOREST-BASED INDUSTRIES

UPM-Kymmene, a Finnish major forest company, is leading the way towards a forest-based bioeconomy with their Biofore program. In Biofore, bioeconomy is coupled with the forest industry, and the ultimate goal is a fossil-free future. Some areas where UPM-Kymmene is active within bioeconomy is biofuels, biocomposites and biochemical. In addition, a biochemical mill is under evaluation in Germany.

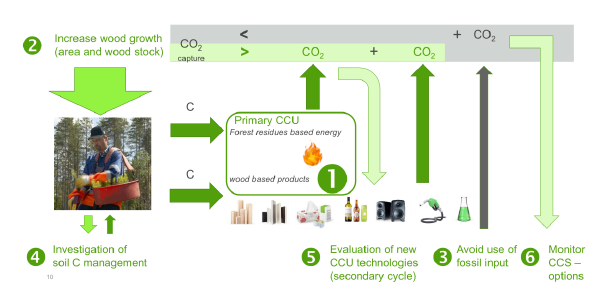

The forest industry is already an established Bio-CCU industry where biomass grown from atmospheric CO2 is used for energy production and wood based products (primary Bio-CCU). As a consequence, the forest industry has a significant responsibility in managing climate change mitigation. The UPM development areas for climate change mitigation are focused on replacing fossil fuel and utilizing renewable energy, including forest residue based energy and wood based products, as illustrated in Figure 14.

Figure 14 UPM activities to mitigate climate change

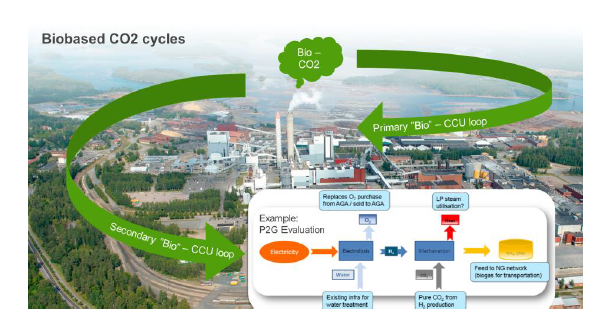

As industrial users of biomass UPM emits significant amounts of biogenic CO2. Utilizing this biogenic CO2 in a secondary Bio-CCU loop for instance for biofuel production such as the illustrated power-to-gas (P2G) example in Figure 15, could be a viable option, but currently this alternative does not offer a potential market with sound market conditions.

Figure 15 Potential Bio-CCU loops for the forest industry

New bio-CCU technologies, such as P2G, could further improve the positive effect on climate change. However, the industry is dependent on business opportunities in order to invest in new technologies such as Bio-CCS and Bio-CCU. Currently there is a significant gap in commercialization of these technologies. In addition, regarding future Bio-CCS, the current EU ETS only covers a small part of CCS, which leaves no incentive for capturing the CO2.

Bio-CCU

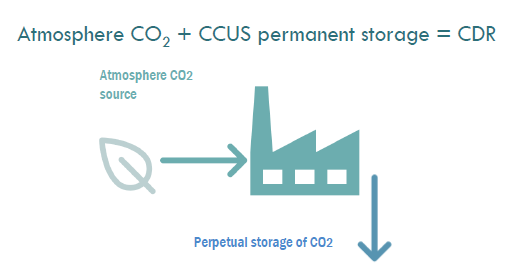

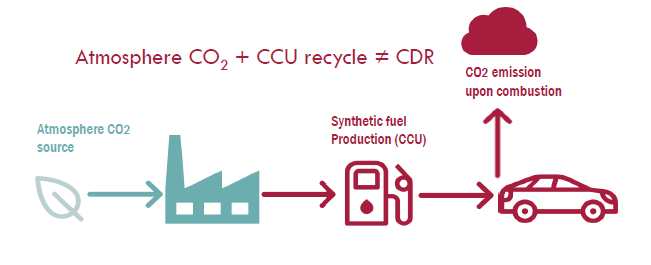

Utilizing captured CO2 as a feedstock in other processes can potentially decrease the rate of fossil carbon extraction. As such, Bio-CCU does not have a direct effect on reducing atmospheric CO2 emissions compared to Bio-CCS. The effect of Bio-CCU on the atmospheric CO2 concentration and hence its efficiency as a climate change mitigation tool depends on the lifecycle of the product produced with captured CO2. In order to effectively mitigate climate change the CO2 should be sequestered in the product for at least decades to centuries. For instance, utilizing atmospheric CO2 for synthetic fuel production to replace fossil fuels cannot be considered a CO2 removal technology as the original CO2 will in most cases not be contained for more than weeks or months before release back into the atmosphere. The difference is illustrated in Figure 16 and Figure 17.

Figure 16 Permanent removal of atmospheric CO2 with Bio-CCS

Figure 16 Permanent removal of atmospheric CO2 with Bio-CCS

Figure 17 Temporary delay in CO2 emission with Bio-CCU

Conclusions

Negative CO2 emissions is currently the only technology that can provide large-scale negative emissions, which are an important part of major future emission scenarios, and indispensable in order to reach climate goals of 2°C and below. Bio-CCUS is not the only solution. A portfolio of CO2 removal technologies will be needed, in the form it makes sense in different regions and communities.

Capturing and storing or utilizing biogenic CO2 is already existing, and plans are underway for new plants to go on-line in the near future. Making Bio-CCUS happen is not primarily about CO2 capture technology, but about systematizing the policy framework around Bio-CCUS and developing transport and storage infrastructure needed for large-scale implementation. In addition, in order for Bio-CCS to offer negative CO2 emissions the biomass utilized must be sustainable, and sustainable biomass for use in Bio-CCUS comes with a limit. Several future GHG emission scenarios operate with unsustainable amounts of biomass.

Currently, there is no incentive for bio-based industry to capture and store CO2. In order to be able to invest in and realize Bio-CCS and negative emissions, some major prerequisites include:

- Policy instruments and market conditions: Accounting for negative emissions in emission trading systems (Bio-CCS) or otherwise enabling the development of business cases (Bio-CCU) will be indispensable for industries to voluntarily invest in carbon negative technologies. Policy instruments should be adaptable to new developments and changes in markets conditions.

- Political stability: Policy instruments that facilitate long-term strategies and build confidence are needed for large-scale investments.

- Defined standards and frameworks: Uncertainties remain among undefined characterizations of Bio-CCS, Bio-CCU and other related terms such as biofuels and sustainable biomaterial. Establishment of common definitions would bring consistency to the discussion.

References

Hannula, I. 2016. Hydrogen enhancement potential of synthetic biofuels manufacture in the European context: A techno-economic assessment. Energy, 104, pp. 199 – 212. DOI: 10.1016/j.energy.2016.03.119

IEA. 2017. Technology Roadmap. Delivering Sustainable Bioenenergy. OECD/IEA, Paris, France.